More Money, Less Stress Approach to Personal Finance Planning.

OBJECTIVES OF FINANCIAL PLANNING

Achieving your dreams - Someday you would like to quit your job and start your own cafe, or a boutique, or do your MBA, or tour the world. If you don't plan for these things, chances are they'll just remain dreams. You will never have the right resources to go about achieving them.

The difference between someone who plans and someone who doesn't, is that the one who plans, puts it into action, whilst the one who doesn't, just talks. You've met these people before. They keep having little crises in their lives, which they claim prevent them from doing what they want. So it is the time for you to take control of your life.List down the things you want to do. Find out how much they cost, and embark on a mission towards achieving the right resources in order to be able to afford them. When your mind is focused this way, you start to be aware of every dollar that you spend and earn. Does it help you achieve your goals? You will have better control of your money, and not be left with very little at the end of every month, and wondering where it all went.

Financial Independence - Can you imagine a time when you are no more a slave to money? When you can do anything you want at any time that you want? The time when you no longer have to work but have enough money not to worry about the major expenses in life, we call that Financial Independence. It's different from retirement. You may still continue to work if you enjoy it. But your have the resources to stop working anytime should you wish to. Financial Independence is different for everybody. It really depends on your lifestyle needs. If you can be happy with small flat, you are likely to reach your Financial Independence sooner than if you have to live in a landed property. Financial Independence doesn't just happen. You have to plan for it. Those who do tend to achieve it sooner than those who don't.

Prudence is a way to achieve the objective - In the book "The Millionaire Next Door: The Surprising Secrets of America's Wealthy" by Thomas J. Stanley and William D. Danko, the authors discovered that the typical American millionaire does not fit the stereo-typical idea of a millionaire. Most of us would think that millionaires are characterized by their big houses, flashy sport cars and expensive jewelry. But what the authors discovered was that most of America's millionaires were average people, living in average houses, driving American-made cars. They tend to have small businesses of their own, and their lives are characterized by long working hours and a high level of prudence in how they spend their money. That's how they amassed their fortune.

So what our parents taught us when we were very young is right. If we work hard and spend little, our chances of making it is a lot higher. If you constantly feel that you need more luxuries in your life, then you may forever be asset-rich, but cash-poor, and certainly a long distance off from financial independence. (Source: FundSupermart)

OBJECTIVES OF FINANCIAL PLANNING

Achieving your dreams - Someday you would like to quit your job and start your own cafe, or a boutique, or do your MBA, or tour the world. If you don't plan for these things, chances are they'll just remain dreams. You will never have the right resources to go about achieving them.

The difference between someone who plans and someone who doesn't, is that the one who plans, puts it into action, whilst the one who doesn't, just talks. You've met these people before. They keep having little crises in their lives, which they claim prevent them from doing what they want. So it is the time for you to take control of your life.List down the things you want to do. Find out how much they cost, and embark on a mission towards achieving the right resources in order to be able to afford them. When your mind is focused this way, you start to be aware of every dollar that you spend and earn. Does it help you achieve your goals? You will have better control of your money, and not be left with very little at the end of every month, and wondering where it all went.

Financial Independence - Can you imagine a time when you are no more a slave to money? When you can do anything you want at any time that you want? The time when you no longer have to work but have enough money not to worry about the major expenses in life, we call that Financial Independence. It's different from retirement. You may still continue to work if you enjoy it. But your have the resources to stop working anytime should you wish to. Financial Independence is different for everybody. It really depends on your lifestyle needs. If you can be happy with small flat, you are likely to reach your Financial Independence sooner than if you have to live in a landed property. Financial Independence doesn't just happen. You have to plan for it. Those who do tend to achieve it sooner than those who don't.

Prudence is a way to achieve the objective - In the book "The Millionaire Next Door: The Surprising Secrets of America's Wealthy" by Thomas J. Stanley and William D. Danko, the authors discovered that the typical American millionaire does not fit the stereo-typical idea of a millionaire. Most of us would think that millionaires are characterized by their big houses, flashy sport cars and expensive jewelry. But what the authors discovered was that most of America's millionaires were average people, living in average houses, driving American-made cars. They tend to have small businesses of their own, and their lives are characterized by long working hours and a high level of prudence in how they spend their money. That's how they amassed their fortune.

So what our parents taught us when we were very young is right. If we work hard and spend little, our chances of making it is a lot higher. If you constantly feel that you need more luxuries in your life, then you may forever be asset-rich, but cash-poor, and certainly a long distance off from financial independence. (Source: FundSupermart)

Financial independent planning is the most challenging kind of planning. It is a long term process planning. Therefore, it is necessary to start from receiving your first pay cheque. While you are making money for the “young you”, you should also start to save in investment planning for the “older you” during your financial independent day.

Wealth Protection is basically to manage your risk (risk management) or in other words it is insurance planning. It is a planning on transferring your risk to a third party (the insurer) to protect your interest. Wealth Protection is to protect against your asset (Property Risk), your financial Catastrophe (Personal Risk) and your wrongdoing to others (Liability Risk).

Wealth Creation & Accumulation start from your first pay cheque. Therefore, you should start to plan for your cash flow and manage your debt in order to save more money for short to medium term purchasing, medium to long term investment planning for your children and for your retirement.

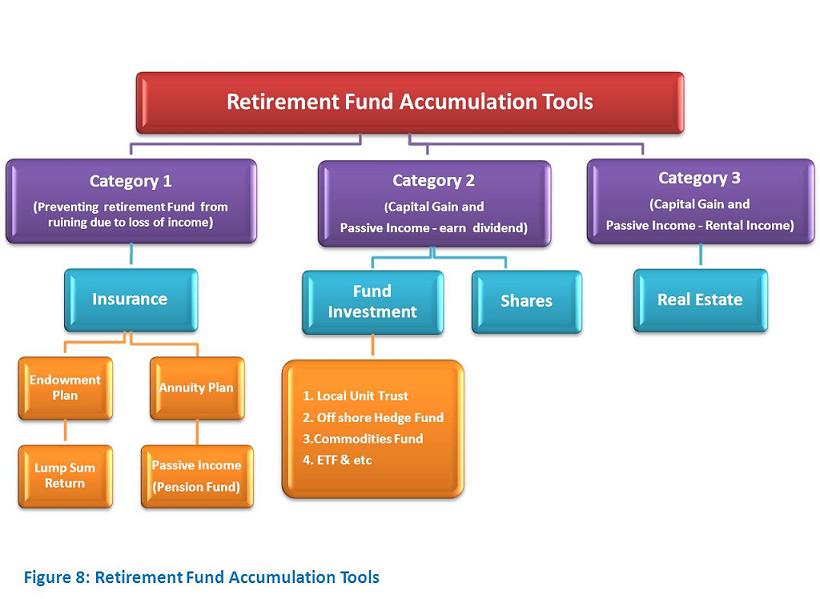

Wealth Conservation is conserving of your investment return and principle after a period of time that you have accumulated your wealth. At any point of time, you should always cautious of inflation. An investment tools that could always hedge against inflation is very much needed especially during your retirement. Wealth Conservation is a challenge during retirement because inflation can eat up your principle amount quietly. In order to be able to conserve more wealth, generating passive income alone is not enough. Investment for capital gain, controlling your expenses, including tax payment, management of cash flow and debt is also very important.

Wealth Distribution - Generally, people will only look into distributing their wealth at their older age. However, based on the financial planning point of view, a person should start to look into one’s Estate Planning when he/she has started to own assets under his/her own name, such as car, property and Fixed Deposit account. Whatever your age, whatever the size of your estate, a proper estate plan will eliminate uncertainties over the administration of a probate (a lengthy and costly legal process that oversees the transfer of assets) and maximize the value of the estate by reducing taxes (as at today Estate Tax is zero in Malaysia) and other expenses.

Wealth Protection is basically to manage your risk (risk management) or in other words it is insurance planning. It is a planning on transferring your risk to a third party (the insurer) to protect your interest. Wealth Protection is to protect against your asset (Property Risk), your financial Catastrophe (Personal Risk) and your wrongdoing to others (Liability Risk).

Wealth Creation & Accumulation start from your first pay cheque. Therefore, you should start to plan for your cash flow and manage your debt in order to save more money for short to medium term purchasing, medium to long term investment planning for your children and for your retirement.

Wealth Conservation is conserving of your investment return and principle after a period of time that you have accumulated your wealth. At any point of time, you should always cautious of inflation. An investment tools that could always hedge against inflation is very much needed especially during your retirement. Wealth Conservation is a challenge during retirement because inflation can eat up your principle amount quietly. In order to be able to conserve more wealth, generating passive income alone is not enough. Investment for capital gain, controlling your expenses, including tax payment, management of cash flow and debt is also very important.

Wealth Distribution - Generally, people will only look into distributing their wealth at their older age. However, based on the financial planning point of view, a person should start to look into one’s Estate Planning when he/she has started to own assets under his/her own name, such as car, property and Fixed Deposit account. Whatever your age, whatever the size of your estate, a proper estate plan will eliminate uncertainties over the administration of a probate (a lengthy and costly legal process that oversees the transfer of assets) and maximize the value of the estate by reducing taxes (as at today Estate Tax is zero in Malaysia) and other expenses.

Types of Financial Planning

There are essentially FOUR main areas of financial planning. The first 3 are covered by us but the last is not. If you need more help with any of the financial planning areas below, please contact the financial planners listed on our site.

1. Insurance Planning: This protects you and your family from extreme financial hardship in the event of any misfortune. As your life situation changes (e.g. when you get married, your kids get older etc.), it is worthwhile to revisit your insurance plan, just to be sure that it covers the additional needs in your life.

2. Investment Planning: This is the proper allocation of your excess cash and savings in the right investment instruments to help you achieve various goals in life, such as buying a house, education, starting a family and so on. The typical investment instruments which Malaysians use are equities, unit trusts, properties, insurance and fixed-interest products.

3. Retirement Planning: EPF alone is not enough for retirement because a large part of it would have been used for the purchase of property. Inflation also eats up the real purchasing power of your EPF savings. Retirement planning involves projecting income growth, estimating the returns of certain investment instruments, planning the amount required to maintain a certain lifestyle after retirement, and so on. This is to be sure that your lifestyle will not suffer greatly once your income stops.

4. Estate and Succession Planning: This involves the allocation of your assets and its implications on taxes, and how you wish to have them transferred or allocated to other parties. Wills, trusts, gifts and other means of estate dutiable items are analyzed. Lawyers and accountants typically feature greatly in these plans.

There are essentially FOUR main areas of financial planning. The first 3 are covered by us but the last is not. If you need more help with any of the financial planning areas below, please contact the financial planners listed on our site.

1. Insurance Planning: This protects you and your family from extreme financial hardship in the event of any misfortune. As your life situation changes (e.g. when you get married, your kids get older etc.), it is worthwhile to revisit your insurance plan, just to be sure that it covers the additional needs in your life.

2. Investment Planning: This is the proper allocation of your excess cash and savings in the right investment instruments to help you achieve various goals in life, such as buying a house, education, starting a family and so on. The typical investment instruments which Malaysians use are equities, unit trusts, properties, insurance and fixed-interest products.

3. Retirement Planning: EPF alone is not enough for retirement because a large part of it would have been used for the purchase of property. Inflation also eats up the real purchasing power of your EPF savings. Retirement planning involves projecting income growth, estimating the returns of certain investment instruments, planning the amount required to maintain a certain lifestyle after retirement, and so on. This is to be sure that your lifestyle will not suffer greatly once your income stops.

4. Estate and Succession Planning: This involves the allocation of your assets and its implications on taxes, and how you wish to have them transferred or allocated to other parties. Wills, trusts, gifts and other means of estate dutiable items are analyzed. Lawyers and accountants typically feature greatly in these plans.

5. EDUCATION PLANNING FOR YOUR CHILDREN

Nowadays, to take an overseas degree course cost you around RM100,000 to RM500,000 a year. A similar course in Malaysia is cheaper, but can still come up to a significant figure. These are current prices, and do not include inflation and future fee increases. There are a number of ways to go about ensuring that you have sufficient funds when your child's university entrance beckons.

1. Bank Time Deposits

2. Stocks

3. IsInvestment-Linked Insurance

4. Unit Trusts

Savings in the bank - We do not recommend that you save your money in the bank to accumulate funds for your child's education. Since you have time on your side, you should invest your savings to get better returns. IMPORTANCE OF SAVINGS - Of all the investment instruments available, savings accounts earn you the lowest returns. Inflation will also reduce the purchasing power of savings over time. Thus, we don't recommend that you keep too much of your money in savings accounts. You should invest it to make greater capital gains.

Savings for Emergencies However, you should keep some money in savings for emergencies. A loved one may fall sick and need extended medical attention, a valuable item at home, like the TV or refrigerator, may break down and - replacement, or a new boss may – make your life miserable and you need to escape from him. If you had all your money in investments, you may find yourself short of cash. If your investments have been making money, you may of course liquidate a part of it to generate the cash that you need. However, you may find that your shortage of cash catches you at a time when all your investments have gone down. Having to liquidate them may cause you to lose even more money. So it is not wise to be over-invested.

Rule of Thumb : - We recommend that you have at least 4 months pay in a savings account. This way, even if you lose your job all of a sudden, you can hold out for 4 months before needing to liquidate your investments.

Protected Principal - Regular Savings Fund

Investors Trust gives you the flexibility of meeting all or part of your children’s educational needs. By working with your financial advisor, you can tailor one of Investors Trust’s plans to suit your goals. We know you want the best for your children. You work hard to make sure they have the finest in life. A quality education is the foundation for your child’s success. It is the best gift you can give your children.

Insurance

This is a way in which to save up for your child's education. Most insurance firms do provide some form of child education cum endowment policy that would mature at the time your child goes to college.

You could also add in the option that if anything happens to you, subsequent premiums for the education plan will not be charged and the plan will still mature at the decided time. This is better than relying on savings because if something unforeseen happens, your savings contribution would have stopped. The downside is that returns are average. Usually, it is barely higher than fixed deposit rate. The good thing though is that you are forced to save, both you and your child are covered by a policy, and you know exactly how much you're going to get back when the policy matures.

Mutual Funds

If you are saving for your child's education in 10 - 15 years time, you have a good time horizon to plan with. You can afford to invest in a unit trust with higher risk which may give you better returns than insurance policies. Choose a fund manager with a good and steady track record.

Rule of Thumb

1. Get a rough idea of how much education will cost by the time when your child attend the university. Local education will probably remain quite affordable. However, the cost of overseas education is less predictable. It depends on the exchange rate and other domestic policies that the local governments might choose to implement.

2. If you really cannot afford to send your children overseas, tell them. If they are really keen on studying abroad, there are many scholarships available to them. All he/she takes is to study hard.

3. Have at least one insurance policy or one unit trust purely dedicated for your child's education. Make sure that your policy does not lapse if you choose the insurance option. If unit trust is the way to go for you, apply for autopay such that your investment becomes automatic.

Good Financial Planning Tips - A good financial plan should include the following:

Nowadays, to take an overseas degree course cost you around RM100,000 to RM500,000 a year. A similar course in Malaysia is cheaper, but can still come up to a significant figure. These are current prices, and do not include inflation and future fee increases. There are a number of ways to go about ensuring that you have sufficient funds when your child's university entrance beckons.

1. Bank Time Deposits

2. Stocks

3. IsInvestment-Linked Insurance

4. Unit Trusts

Savings in the bank - We do not recommend that you save your money in the bank to accumulate funds for your child's education. Since you have time on your side, you should invest your savings to get better returns. IMPORTANCE OF SAVINGS - Of all the investment instruments available, savings accounts earn you the lowest returns. Inflation will also reduce the purchasing power of savings over time. Thus, we don't recommend that you keep too much of your money in savings accounts. You should invest it to make greater capital gains.

Savings for Emergencies However, you should keep some money in savings for emergencies. A loved one may fall sick and need extended medical attention, a valuable item at home, like the TV or refrigerator, may break down and - replacement, or a new boss may – make your life miserable and you need to escape from him. If you had all your money in investments, you may find yourself short of cash. If your investments have been making money, you may of course liquidate a part of it to generate the cash that you need. However, you may find that your shortage of cash catches you at a time when all your investments have gone down. Having to liquidate them may cause you to lose even more money. So it is not wise to be over-invested.

Rule of Thumb : - We recommend that you have at least 4 months pay in a savings account. This way, even if you lose your job all of a sudden, you can hold out for 4 months before needing to liquidate your investments.

Protected Principal - Regular Savings Fund

Investors Trust gives you the flexibility of meeting all or part of your children’s educational needs. By working with your financial advisor, you can tailor one of Investors Trust’s plans to suit your goals. We know you want the best for your children. You work hard to make sure they have the finest in life. A quality education is the foundation for your child’s success. It is the best gift you can give your children.

Insurance

This is a way in which to save up for your child's education. Most insurance firms do provide some form of child education cum endowment policy that would mature at the time your child goes to college.

You could also add in the option that if anything happens to you, subsequent premiums for the education plan will not be charged and the plan will still mature at the decided time. This is better than relying on savings because if something unforeseen happens, your savings contribution would have stopped. The downside is that returns are average. Usually, it is barely higher than fixed deposit rate. The good thing though is that you are forced to save, both you and your child are covered by a policy, and you know exactly how much you're going to get back when the policy matures.

Mutual Funds

If you are saving for your child's education in 10 - 15 years time, you have a good time horizon to plan with. You can afford to invest in a unit trust with higher risk which may give you better returns than insurance policies. Choose a fund manager with a good and steady track record.

Rule of Thumb

1. Get a rough idea of how much education will cost by the time when your child attend the university. Local education will probably remain quite affordable. However, the cost of overseas education is less predictable. It depends on the exchange rate and other domestic policies that the local governments might choose to implement.

2. If you really cannot afford to send your children overseas, tell them. If they are really keen on studying abroad, there are many scholarships available to them. All he/she takes is to study hard.

3. Have at least one insurance policy or one unit trust purely dedicated for your child's education. Make sure that your policy does not lapse if you choose the insurance option. If unit trust is the way to go for you, apply for autopay such that your investment becomes automatic.

Good Financial Planning Tips - A good financial plan should include the following:

- A comprehensive solution that covers all of your financial needs

- Product structure that allows your investments to grow tax free

- Flexibility in contributions to allow for changes in lifestyle

- A complete choice of investment alternatives

- Liquidity and access to capital

- Insurance protection for you and your family

- Security from global diversification and hedge currencies risks