It was a FANTASTIC BUDGET 2014 presented recently. Many rich business people are very happy indeed and many poor people cried too after the announcement of the entire cut of sugar subsidy and the forthcoming Goods and Services Tax (GST) set at 6% starting 1 April 2015. The Opposition politicians say "A RICH Man's Budget" and we recalled the past "People Budget " launched when the ruling party won handsomely in GE11. It is not a proper time to debate about who is right or who is wrong here, but overall we can see the medium income workers and poor people will be affected mostly from the domino effect of rising cost of living, deficit budget, high household debts and inflation hike.

Frankly speaking, the coming GST set at 6% p.a. as a consumption tax commencing on 1 April 2015 will really hurt our pockets especially the middle income workers and the poor people too. Yes, we know that GST will replace the existing double taxes from sales tax and service tax that the business people cannot claim their refund but absorbed by the consumers like us. Now we get lesser tax from GST system as long as we keep a low consumption everyday. In short, please cut down on our daily expenses and also don't go shopping sprees and less expenditures

on outside foods, entertaining, changing new cars, cloths, electronic gadgets and etc. No one can predict the actual impact of GST amount will reduce our savings each month but it depends on our consumption habits and lifestyle now and in future.

The Bad Taxes & The Good Taxes - Your Choices Now

Based on the announced Budget 2014, it is too early for us to determine the segregation of the bad taxes and the good taxes. However, it is our choices now to choose the appropriate taxes that can affect their pockets seriously. We have identified several main core taxes that really relevant to our wealth management and financial planning activities as mentioned below.

1. Real Property Gain Tax (RPGT)

To increase the ability of the rakyat to buy a house and ensure stable house prices, as well as to control excessive speculative activities, the Government will implement the following steps :

First: Review Real Property Gains Tax (RPGT). For gains on properties disposed within the holding period of up to 3 years, RPGT rate is

increased to 30%, whereas for disposals within the holding period up to 4 and 5 years, the rates are increased to 20% and 15%, respectively. For disposals made in the sixth and subsequent years, no RPGT is imposed on citizens, whereas companies are taxed at 5%.

For non-citizens, RPGT is imposed at 30% on the gains from properties disposed within the holding period of up to 5 years and for disposals in the sixth and subsequent years, RPGT is imposed at 5%.

Second: Increase the minimum price of property that can be purchased by foreigners from RM500,000 to RM1,000,000;

Third: Increase transparency in property sales price, where property developers will have to display detailed sales price including all benefits and

incentives offered to buyers such as exemption of legal fees, stamp duty, sales agreements, cash rebates and free gifts; and

Fourth: Prohibit developers from implementing projects that have features of Developer Interest Bearing Scheme (DIBS), to prevent developers from incorporating interest rates on loans in house prices during the construction period. Therefore, financial institutions are prohibited from providing final funding for projects involved in the DIBS scheme.

Well, the property speculators and punters will be crying very loud soon when they cant flip flop their completed new properties in coming months. If they cant rent them out is also a big problem, so they will also face RPGT set at 30%, 20% and 15% respectively based on the holding years are damn painful since new expensive properties cannot gain capital appreciation more than 15% to 30% in the first 3 years. Can a property speculator does it ? Foreign investors will also stay out from the property investment due to a very high purchase price of entry at RM1.0 million above and a costly single tier RPGT at 30% exit level. Do the foreign investors agree ? We wish them all the best luck in their property investment in Malaysia.

2. Private Retirement Scheme (PRS)

The Government recognizes the importance of savings from an early age to ensure sufficient savings after retirement. To further increase savings, the Government encourages youth to undertake long-term investment through the Private Retirement Scheme (PRS).

3. Empowering Bumiputeras

To increase Bumiputera equity ownership, SME Bank will establish Bumiputera Equity Fund (EquiBumi) with an allocation of RM300 million to provide loans to credible Bumiputera companies to take over listed companies or companies with potential to be listed on Bursa Malaysia.

We expect the bullish FBM KLCI will hike above 1,900 points to 2,000 points in 2014 onwards since the increase volume of Bumiputera companies participation in the stock market now. Timely to snap up more Shariah stocks and value added blue chip stocks by all stock investors and fund managers.

4. Tax incentives

5. Goods and Services Tax (GST)

The Government proposes that the sales tax and service tax be abolished. These two taxes will be replaced by a single tax known as the Goods and Services Tax (GST). Currently, the inflation rate is low at 2%. The Government believes that this is the best time to implement GST as the inflation rate is low and contained. With the implementation of GST, the Government will be able to address the weaknesses in the current taxation system. The GST rate is fixed at 6% and to be effective from 1 April 2015, approximately 17 months from today.

The “long-overdue” GST unveiled by Prime Minister Datuk Seri Najib Tun Razak in Budget 2014 has received the thumbs up from economists and tax experts. Conversely, a knee-jerk reaction in the opposite direction could take place right after GST is implemented, which might see consumers refraining from discretionary purchases or spending less. It's an April Fool GTS ?

Last but not least, you should consider the points and read the 4 signs' advices below:-

4 SIGNS THAT YOUR FINANCIAL HEALTH IS SUFFERING.

Sometimes we look at people in financial trouble and wonder how they ever got to that point. We think, “That will never happen to me.”

The thing is, debt is one of those things that sneaks up and when you finally realize you’re at that point, it’s too late. We need to identify these “symptoms” of “financial sickness” early so we can get early “financial treatment” and start working towards being financially healthy.

# 1. YOU ARE ALWAYS DISCONTENT.

Do you find yourself constantly wanting more? Is it a challenge to watch your friends and relatives upgrade to nicer cars, bigger homes, better furniture or even more expensive independent schools for children? If you’re quietly saying yes, then your discontentment may be driving you to impulsive financial decisions.

#2. YOU CAN'T AFFORD TO LOSE YOUR INCOME.

If you or your spouse lost your income, would you be able to survive for 6 months only on what you have set aside in your savings? If the answer is NO, or if you’re unsure, you may be overspending on today’s wants while sacrificing tomorrow’s needs.

#3 CREDIT IS YOUR BEST FRIEND - OR SO YOU THINK.

Is your monthly credit card balance growing instead of declining? Do you use one card to pay off another? If the answer is yes, then you are likely living beyond your means.

#4 YOU DON'T HAVE A WRITTEN PLAN TO MANAGE YOUR MONEY.

Saving is the foundation of healthy finances, yet so few of us actually save. One of the most common excuse for not saving is “I have too much debt.” What people don’t realize is that, unless they prioritize putting money aside, debt will always be an issue.

Frankly speaking, the coming GST set at 6% p.a. as a consumption tax commencing on 1 April 2015 will really hurt our pockets especially the middle income workers and the poor people too. Yes, we know that GST will replace the existing double taxes from sales tax and service tax that the business people cannot claim their refund but absorbed by the consumers like us. Now we get lesser tax from GST system as long as we keep a low consumption everyday. In short, please cut down on our daily expenses and also don't go shopping sprees and less expenditures

on outside foods, entertaining, changing new cars, cloths, electronic gadgets and etc. No one can predict the actual impact of GST amount will reduce our savings each month but it depends on our consumption habits and lifestyle now and in future.

The Bad Taxes & The Good Taxes - Your Choices Now

Based on the announced Budget 2014, it is too early for us to determine the segregation of the bad taxes and the good taxes. However, it is our choices now to choose the appropriate taxes that can affect their pockets seriously. We have identified several main core taxes that really relevant to our wealth management and financial planning activities as mentioned below.

1. Real Property Gain Tax (RPGT)

To increase the ability of the rakyat to buy a house and ensure stable house prices, as well as to control excessive speculative activities, the Government will implement the following steps :

First: Review Real Property Gains Tax (RPGT). For gains on properties disposed within the holding period of up to 3 years, RPGT rate is

increased to 30%, whereas for disposals within the holding period up to 4 and 5 years, the rates are increased to 20% and 15%, respectively. For disposals made in the sixth and subsequent years, no RPGT is imposed on citizens, whereas companies are taxed at 5%.

For non-citizens, RPGT is imposed at 30% on the gains from properties disposed within the holding period of up to 5 years and for disposals in the sixth and subsequent years, RPGT is imposed at 5%.

Second: Increase the minimum price of property that can be purchased by foreigners from RM500,000 to RM1,000,000;

Third: Increase transparency in property sales price, where property developers will have to display detailed sales price including all benefits and

incentives offered to buyers such as exemption of legal fees, stamp duty, sales agreements, cash rebates and free gifts; and

Fourth: Prohibit developers from implementing projects that have features of Developer Interest Bearing Scheme (DIBS), to prevent developers from incorporating interest rates on loans in house prices during the construction period. Therefore, financial institutions are prohibited from providing final funding for projects involved in the DIBS scheme.

Well, the property speculators and punters will be crying very loud soon when they cant flip flop their completed new properties in coming months. If they cant rent them out is also a big problem, so they will also face RPGT set at 30%, 20% and 15% respectively based on the holding years are damn painful since new expensive properties cannot gain capital appreciation more than 15% to 30% in the first 3 years. Can a property speculator does it ? Foreign investors will also stay out from the property investment due to a very high purchase price of entry at RM1.0 million above and a costly single tier RPGT at 30% exit level. Do the foreign investors agree ? We wish them all the best luck in their property investment in Malaysia.

2. Private Retirement Scheme (PRS)

The Government recognizes the importance of savings from an early age to ensure sufficient savings after retirement. To further increase savings, the Government encourages youth to undertake long-term investment through the Private Retirement Scheme (PRS).

- To allocate RM210 mil for a private retirement scheme (PRS) to encourage young to start saving. Starting Jan 1, 2014 the government will top up RM500 into the account for those aged 20-30 years old who can save RM1,000.

- Entitlement for tax rebate up to RM780 for PRS invested at RM3,000 per year

3. Empowering Bumiputeras

To increase Bumiputera equity ownership, SME Bank will establish Bumiputera Equity Fund (EquiBumi) with an allocation of RM300 million to provide loans to credible Bumiputera companies to take over listed companies or companies with potential to be listed on Bursa Malaysia.

We expect the bullish FBM KLCI will hike above 1,900 points to 2,000 points in 2014 onwards since the increase volume of Bumiputera companies participation in the stock market now. Timely to snap up more Shariah stocks and value added blue chip stocks by all stock investors and fund managers.

4. Tax incentives

- In tandem with GST, individual income tax rates to be reduced by one to three percentage points for all taxpayers

- Chargeable income subject to maximum rate to be increased from exceeding RM100,000 to exceeding RM400,000.

- Current maximum tax rate at 26% to be reduced to 24%, 24.5% and 25%. These measures to be effective from 2015.

- Tax rebate of RM2,000 for those earning less than RM8,000

- To help the employer's burden of implementing of minimum wage scheme - RM900 in Peninsula Malaysia and RM800 in Sabah and Sarawak, the government will introduce extra tax incentives for whole of 2014. This is to help employers to top up salaries of their employees to the minimum level.

- Corporate tax rate cut by 1 percentage point from 25% to 24%, for SMEs reduction from 20% to 19% from year of assessment 2016.

- Cooperative tax rate cut by 1 to 2 percentage points from year of assessment 2015

5. Goods and Services Tax (GST)

The Government proposes that the sales tax and service tax be abolished. These two taxes will be replaced by a single tax known as the Goods and Services Tax (GST). Currently, the inflation rate is low at 2%. The Government believes that this is the best time to implement GST as the inflation rate is low and contained. With the implementation of GST, the Government will be able to address the weaknesses in the current taxation system. The GST rate is fixed at 6% and to be effective from 1 April 2015, approximately 17 months from today.

The “long-overdue” GST unveiled by Prime Minister Datuk Seri Najib Tun Razak in Budget 2014 has received the thumbs up from economists and tax experts. Conversely, a knee-jerk reaction in the opposite direction could take place right after GST is implemented, which might see consumers refraining from discretionary purchases or spending less. It's an April Fool GTS ?

Last but not least, you should consider the points and read the 4 signs' advices below:-

4 SIGNS THAT YOUR FINANCIAL HEALTH IS SUFFERING.

Sometimes we look at people in financial trouble and wonder how they ever got to that point. We think, “That will never happen to me.”

The thing is, debt is one of those things that sneaks up and when you finally realize you’re at that point, it’s too late. We need to identify these “symptoms” of “financial sickness” early so we can get early “financial treatment” and start working towards being financially healthy.

# 1. YOU ARE ALWAYS DISCONTENT.

Do you find yourself constantly wanting more? Is it a challenge to watch your friends and relatives upgrade to nicer cars, bigger homes, better furniture or even more expensive independent schools for children? If you’re quietly saying yes, then your discontentment may be driving you to impulsive financial decisions.

#2. YOU CAN'T AFFORD TO LOSE YOUR INCOME.

If you or your spouse lost your income, would you be able to survive for 6 months only on what you have set aside in your savings? If the answer is NO, or if you’re unsure, you may be overspending on today’s wants while sacrificing tomorrow’s needs.

#3 CREDIT IS YOUR BEST FRIEND - OR SO YOU THINK.

Is your monthly credit card balance growing instead of declining? Do you use one card to pay off another? If the answer is yes, then you are likely living beyond your means.

#4 YOU DON'T HAVE A WRITTEN PLAN TO MANAGE YOUR MONEY.

Saving is the foundation of healthy finances, yet so few of us actually save. One of the most common excuse for not saving is “I have too much debt.” What people don’t realize is that, unless they prioritize putting money aside, debt will always be an issue.

Most people go through life lacking the financial education, the knowledge and the skills to build wealth... especially in a "slowing" economy and high taxes like personal income tax and GST - consumption tax over your head till you die with no escape. Economists and analysts expect more adjustments in petrol prices next year 2014, in line with the Government’s subsidy rationalisation plan after the abolishment of sugar subsidy, which aims to lighten the burden on the country’s fiscal deficit. Tough times call for tough measures. It takes political will and courage to invoke the necessary bitter medicine such as the GST implementation and sugar subsidy rationalisation. These tough measures indeed not easily acceptable and managed by the people who fail to plan ahead their wealth management and financial planning.

(Budget 2014 - Reference sources from The STAR paper)

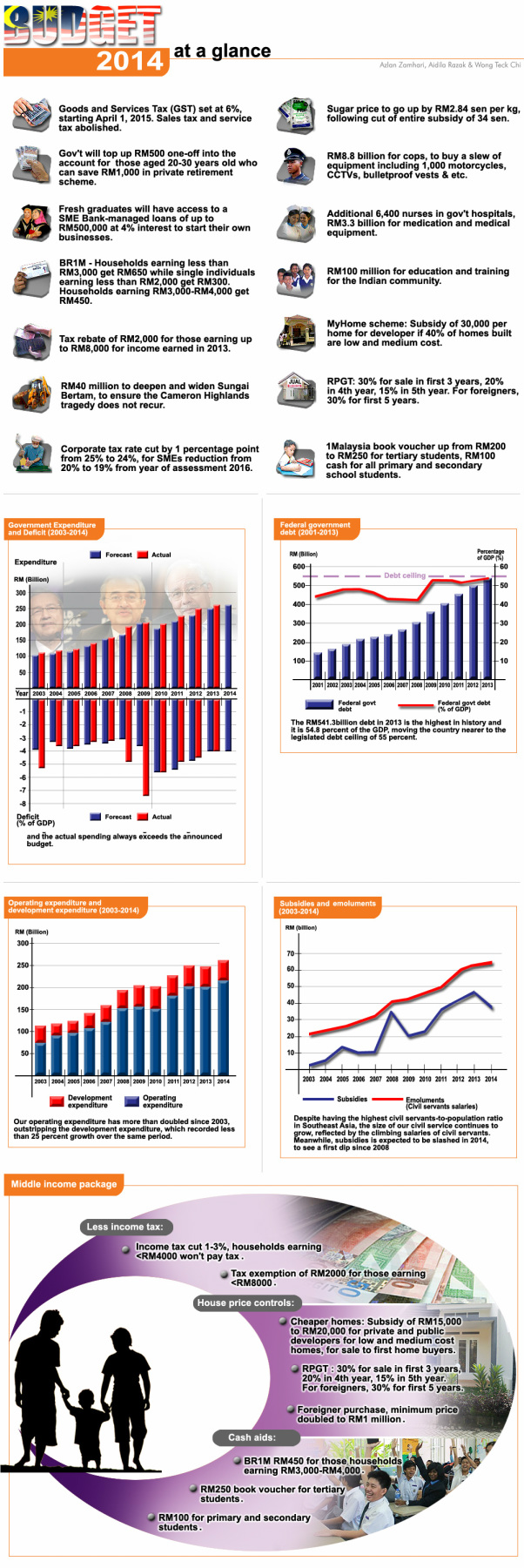

Below is Budget 2014 at a glance.

(Budget 2014 - Reference sources from The STAR paper)

Below is Budget 2014 at a glance.